Stock Market Update Tuesday July 8, 2025

Stock Market Update Tuesday July 8, 2025 Markets Pause Amid Trade Jitters & Yield Stability U.S. equity indices traded sideways as risk appetite cooled, with the S&P 500 oscillating within a tight 25-point intraday range, reflecting a lack of directional conviction. Beneath the surface, sector rotation and idiosyncratic volatility persisted. Financials underperformed sharply, particularly the banking sector, while small-cap equities staged a modest rebound, suggesting tentative risk reallocation.

In fixed income, the long bond edged higher, with 30-year Treasury yields rising 2 basis points to 4.94%, while the 2-year note held steady at 3.90%, flattening the yield curve further and reinforcing market expectations for a prolonged policy hold.

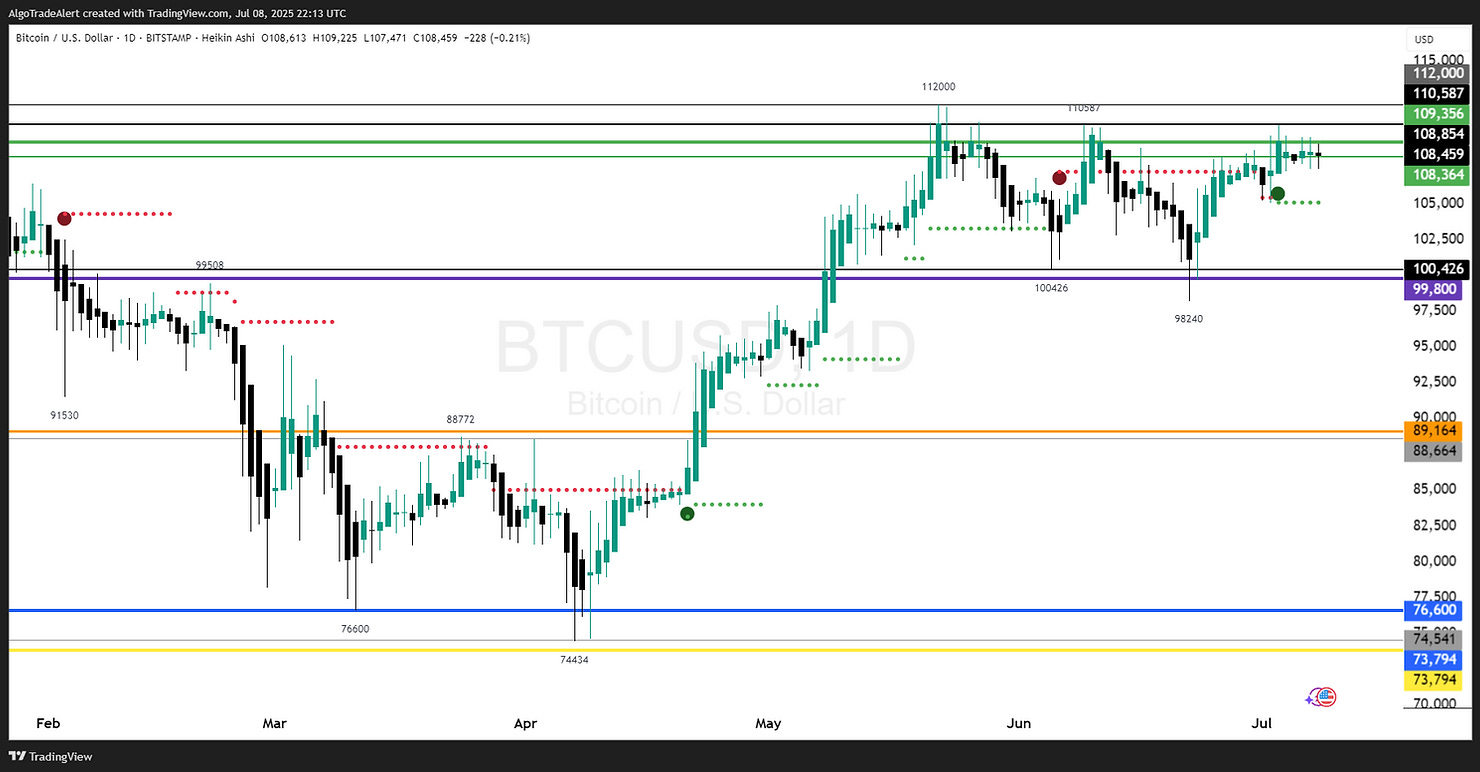

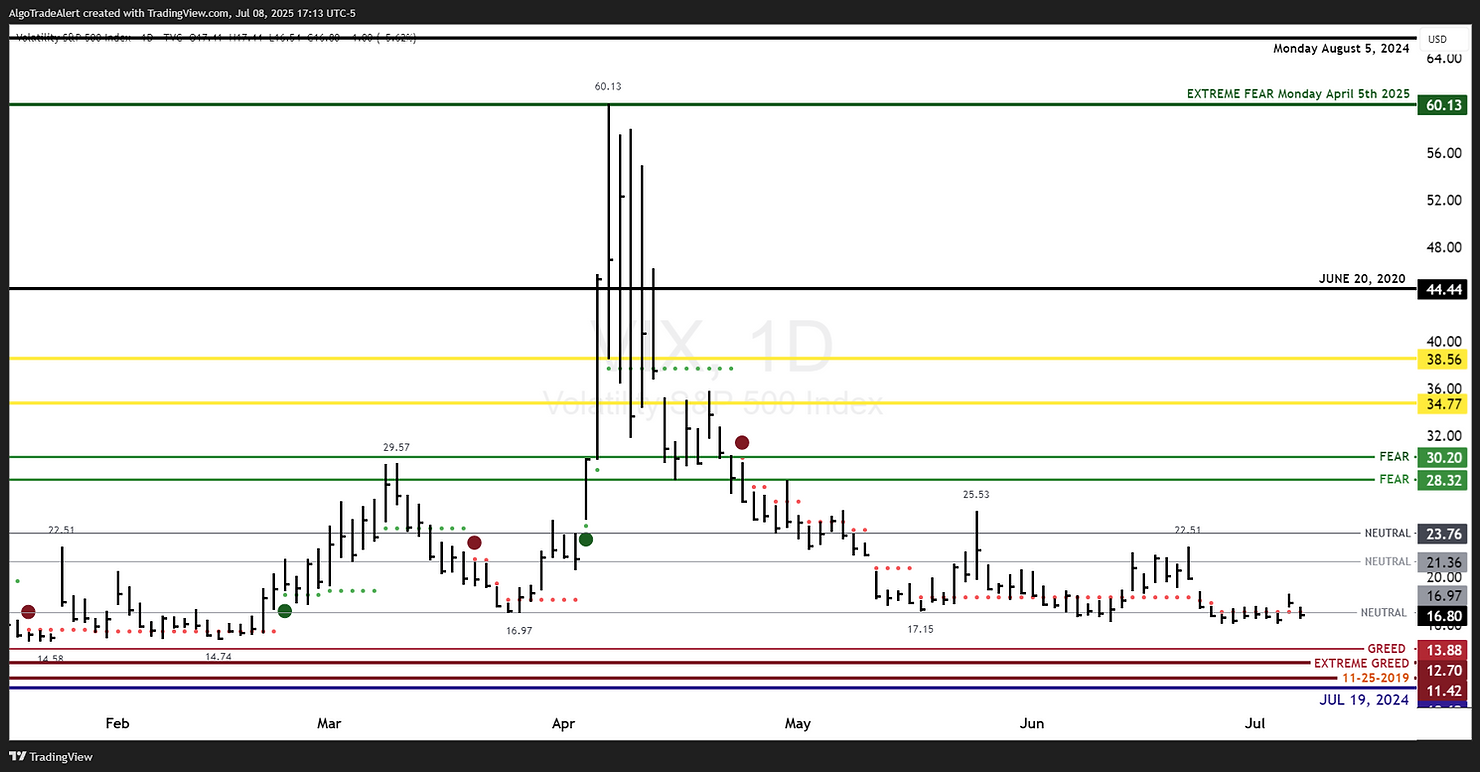

Commodities traded mixed. WTI crude breached $68 per barrel on supply concerns, while gold retreated to $3,302/oz amid lower demand for safe havens. Bitcoin extended its rally toward the $109,000 mark, and implied volatility receded, with the VIX slipping below the 17 handle.

Trade Tensions Cloud Sentiment: Tariff Uncertainty Pressures Equities

Equity markets struggled for traction following President Trump’s announcement of sharply higher tariffs on 14 countries, scheduled to take effect August 1. The S&P 500 finished marginally lower (-0.07%), while the Dow Jones Industrial Average led the downside, closing off 0.36%. Investor sentiment whipsawed as initial risk-off flows subsided when Trump signaled the deadline was “firm but not 100% firm,” leaving open the potential for diplomatic concessions. This nuanced shift preserved hopes for trade negotiations, keeping the broader indices near record territory.

Market Breadth Narrows: A Structural Warning?

Despite the S&P 500 hovering near all-time highs, breadth remains thin, with a shrinking pool of constituents driving the rally. Strategists are increasingly concerned that the concentration of gains in megacap names may signal fragility beneath headline strength. Should leadership fail to broaden, downside risks may intensify.

Sector Performance: Tech and Healthcare Provide Cushion

Sector dispersion was notable. Technology and healthcare names provided ballast, offsetting material weakness in financials and consumer discretionary stocks. Intel surged 7.7% on favorable guidance and product momentum, while major banks like JPMorgan Chase and Bank of America declined over 2%, pressured by trade tensions and elevated long-end yields.

Looking Ahead: Light Macro Calendar, Earnings in Focus

The coming week features a sparse macroeconomic docket. Wednesday’s dual catalysts—extension of reciprocal tariffs and the release of the June FOMC minutes—could provide directional cues. Fed communication remains limited, with only one voting member scheduled to speak. In corporate news, Delta Air Lines is set to report earnings on Thursday, offering insights into travel demand and inflation pass-through dynamics.

Bottom Line:

Broad-Based Technical Strength Suggests Constructive Outlook

With all five major U.S. equity indices currently registering weekly buy signals, the market setup remains structurally bullish. We anticipate any pullbacks to be shallow and met with swift dip-buying activity, reinforcing the prevailing uptrend. The breadth of participation is particularly notable—broad sector rotation and upside momentum are supporting the latest push to all-time highs for the S&P 500 (SPX) and Nasdaq-100 (QQQ), with both the Dow Jones Industrial Average (DJIA) and equal-weighted S&P 500 (RSP) positioned to potentially confirm new highs in the coming week.

This type of broad-based expansion across market cap and sector exposures strengthens the bull case and suggests durable internal support for the rally.

Sentiment is gradually shifting, with investors beginning to re-engage and increase risk exposure. While this uptick in optimism reflects growing confidence in the trend, current positioning and sentiment readings are not yet at levels typically associated with euphoria or overbought extremes. As such, we do not yet see the conditions necessary for a market top, but sentiment will remain a key variable to monitor in the sessions ahead.

The S&P 500 Equal Weight ETF (RSP) signaled a buy alert for the weekly chart on Thursday July 3, 2025 chart; now we have all five major indexes with confirmed buy signals on both a daily and weekly basis. Our next W.D. Gann Cycle Pivot Date will be released later this month. You can find out more in our premium Discord channel.

On June 9, 2025 Our proprietary algorithm has issued weekly buy signals across four of the five major U.S. equity benchmarks—the S&P 500 (SPY), Nasdaq-100 (QQQ), Russell 2000 (IWM), and Dow Jones Industrial Average (DIA). Tuesday, April 29, 2025, we have IWM & RSP ETFs; the two are the most important indexes to give buy signals. Now, we have all five major indexes with buy signals generated from our proprietary algorithm. Monday, April 28, 2025, we had a buy signal generated from our proprietary algorithm for the Dow Jones ETF DIA on the daily chart. The market structure continues to improve, breadth thrusts confirm internal strength, and technical conditions suggest that while short-term upside could be capped, the path of least resistance remains higher. April 25, 2025 Technical Outlook: SPY, QQQ, and DIA have daily buy signals. Sector ETFs (XLK, AIQ, SMH, XLY) have triggered buy signals. April 24, 2025, VIX has a daily sell signal (bullish for equities), as do Bitcoin.